10.5 Stochastic Column Parameters for Bayesian BF

BF above uses stochastic row parameters \(x_i\) and deterministic column parameters (Vol. Wtd. average LDFs)

We can use stochastic process for both by first estimating the column parameters then the row parameters

Define improper prior distribution for the column parameters first before applying prior distributions for the row parameters and estimating them

This approach allows us to take into account the fact that the column parameters have been estimated when calculating the prediction errors, predictive distribution etc

We don’t have to include any information about the column parameters so we use improper gamma distribution (wide variance) for the column parameters

Result posterior distribution:

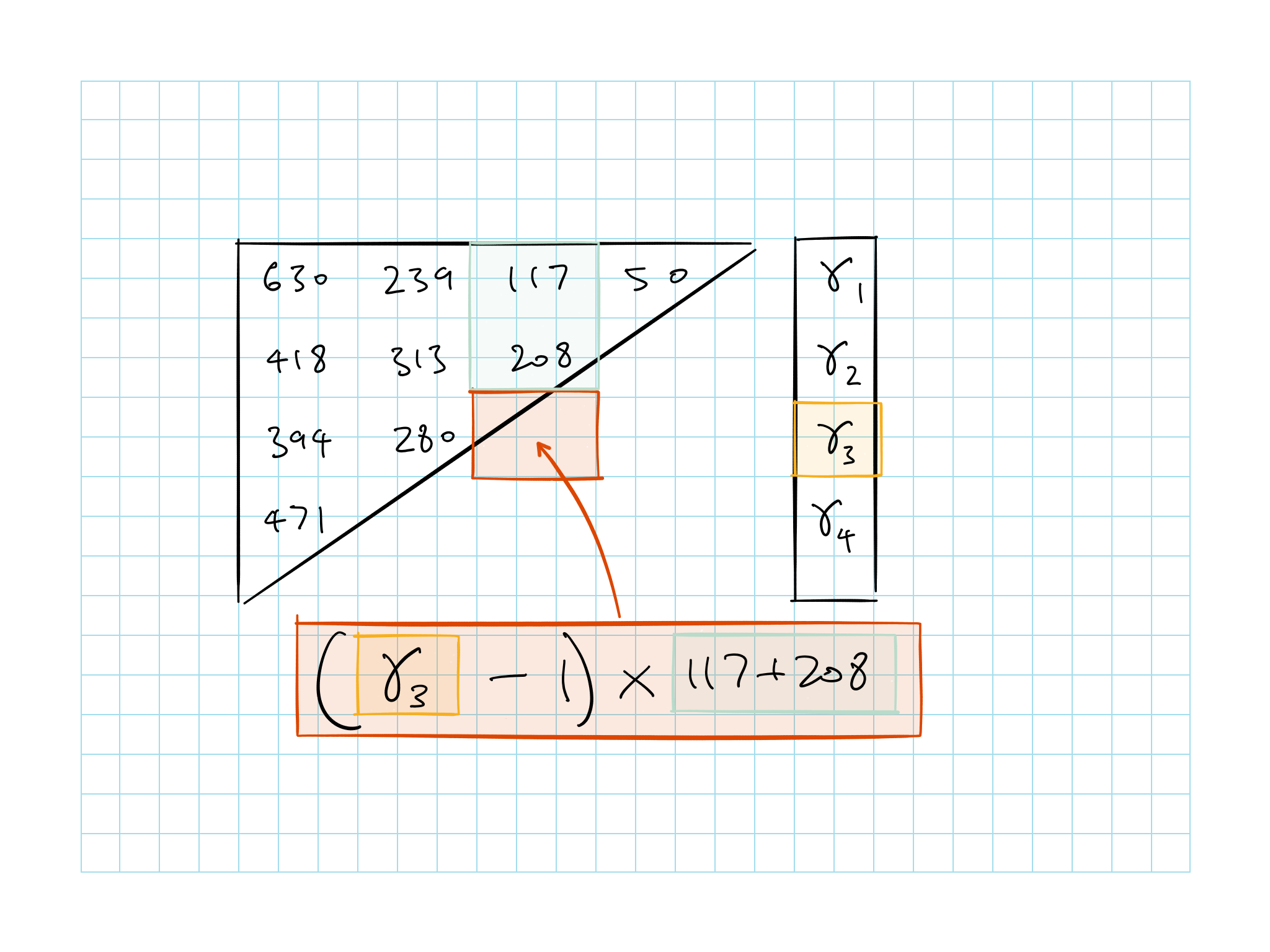

\[\begin{equation} \begin{array}{c} c_{ij} \mid c_{1,j}, c_{2,j},..., c_{i-1,j}, x, \varphi \sim ODNB \\ \mathrm{E}[c_{ij}] = (\gamma_i - 1) \sum \limits_{m=1}^{i-1} c_{m,j} \\ \end{array} \tag{10.13} \end{equation}\]Note that it is similar to (10.6) but recursive down the column (over \(i\))

- \(\sum \downarrow\)

\(\gamma_i\) is the new row parameters

- This tells you the level of losses in the row relative to the rows above

Figure 10.1: Stochastic Column Parameters

We now have a stochastic version of the BF method

BF inserts values for the expected ultimate claims in each row, \(x_i\), in the form of the values \(M_i\)

In Bayesian context, prior distributions will be defined for the parameters \(x_i\) as discussed above

However, the model has been reparameterized with a new set of parameters \(\gamma_i\)

Therefore it is necessary to define the relationship between the new parameters \(\gamma_i\) and the original \(x_i\)

Section below shows how to find \(\gamma_i\) from the values of \(x_i\) given in the prior distributions

Stochastic BF summary:

Column parameters (LDFs) are dealt with first using improper prior

Their estimates will be those implied by the Chainladder

Prior information can be defined in terms of distributions for the parameters \(x_i\), which can then be converted into values for the parameters \(\gamma_i\)

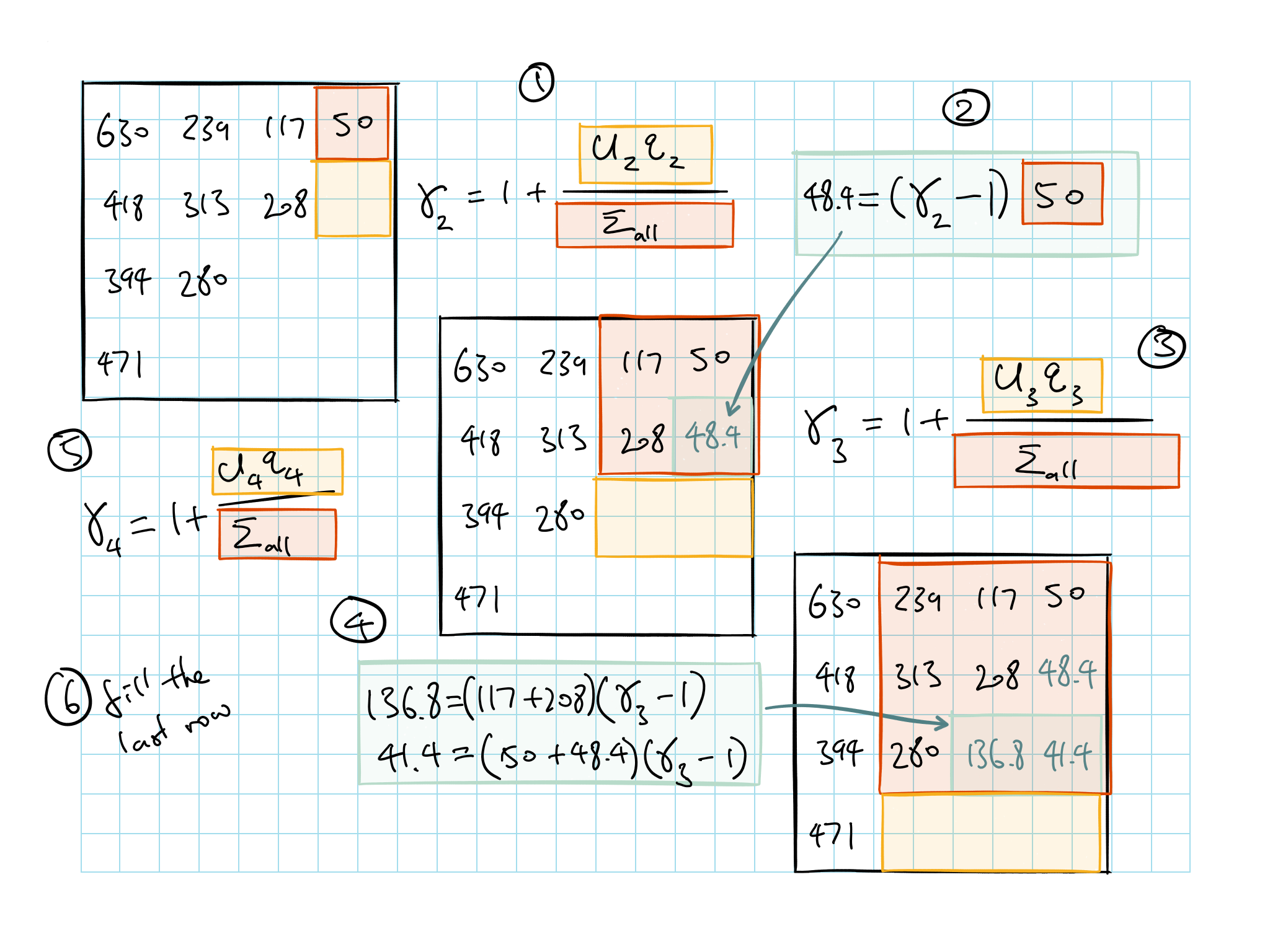

10.5.1 Calculate Gamma

Know how to calculate this pictorially (equation is complicated…)

First, use Chainladder to get ultimate loss and % unpaid by AY

\[\gamma_1 = 1.000\]

First calculate LDFs, then the % unpaid and a-priori for each AY

\(U_i\) = a-priori ultimate based on LDF for AY \(i\)

\(q_i\) = % unpaid for AY \(i\)

Figure 10.2: Calculating gamma

Note that in step 4 above if you don’t need the individual cells you can just take the \(U_3 q_3\)